Table Of Content

While the lender pulls the report on their own, it’s wise to review your credit score beforehand to make sure you’re in a good position to qualify for a loan and to spot and fix any errors, if necessary. You may also be required to include the names and contact information of the landlords you’ve had previously. This will help the lender verify that you’ve upheld your financial responsibilities as a tenant. How far back you’ll need to show payments or landlord information may depend on your lender. Lenders want to be assured you’ll make your monthly mortgage payments on time. If you’re a renter, you’ll likely be required to show that you’ve made on-time rent payments in the past.

How We Make Money

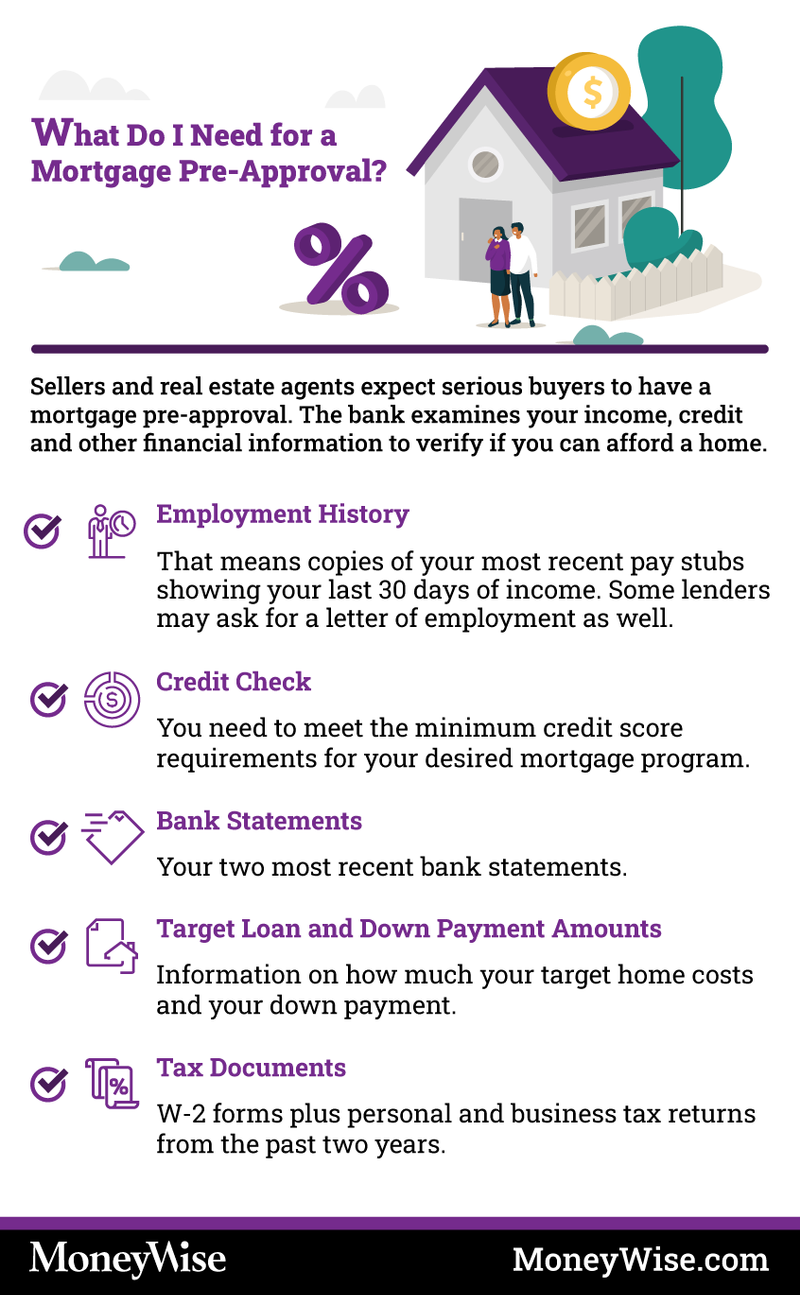

You’ll want to be preapproved before you make an offer on a home, and then apply for full approval once you have a purchase agreement in place. Additionally, be prepared to provide pay stubs indicating your current income and employment status. As a home buyer, it’s crucial for you to be aware that the validity of a mortgage preapproval typically ranges from 60 to 90 days. If your preapproval expires before you find a suitable property or make an offer, prompt communication with your lender becomes essential. You’ll also be asked to provide salary information, so a lender has evidence that you earn enough money to afford a mortgage payment and related monthly housing expenses. You’ll also have to provide 60 days (and possibly more, if you’re self-employed) of bank statements to show that you have enough cash at hand for a down payment and closing costs.

How is a pre-approval different from final loan approval?

When a seller accepts an offer on their house, the buyer will complete at least one full mortgage loan application. The terms, including fees and other costs, may differ in the estimate documents that the buyer receives from the lender. This is why it’s crucial to avoid any financial moves after preapproval that could make you appear riskier to lenders. Things not to do during mortgage preapproval include applying for new credit, making large purchases or missing loan and credit card payments.

Will I get approved for a mortgage with bad credit?

The offers that appear on this site are from companies that compensate us. But this compensation does not influence the information we publish, or the reviews that you see on this site. We do not include the universe of companies or financial offers that may be available to you.

Pre-approval Process

Here’s a checklist of everything you’ll need to get approved for a home loan. And, of course, if you switch lenders, you’ll need to provide the whole lot. You don’t have to stay with the lender that gave you pre-approval, so you can consider applying elsewhere, which is a good idea in any case. Form 4506 is used to request a copy of your tax return directly from the IRS, thus preventing you from submitting falsified returns to the lender. It costs $43 per return, but you may be able to request Form 4506-T for free. Form 8821 authorizes your lender to go to an IRS office and examine the forms you designate for the years you specify, free of charge.

Pre-approvals include a credit report, and one-in-three reports contain errors. Preapproval letters are valid for a specific period, so don’t wait too long after receiving your preapproval to go house-hunting. If your financial situation changes drastically or the home you want doesn’t pass an inspection, you might not get the mortgage you were preapproved for. Many mortgage preapprovals are valid for 90 days, though some lenders will only authorize a 30- or 60-day preapproval.

Mortgage Calculators

Others are more tech-focused and offer a convenient, online mortgage lending process. If your mortgage preapproval expires, it means the lender’s evaluation of your financial standing is no longer current. In such cases, promptly communicate with your lender, as they may require updated financial documentation for reevaluation. If not granted, you may need to initiate the preapproval process anew, emphasizing the importance of swift action to prevent delays in your home buying journey. In your mortgage preapproval journey, factors like your credit score, DTI and income play a pivotal role in determining the approved borrowing amount for your house. A higher credit score indicates greater creditworthiness, often resulting in a more favorable mortgage terms.

Get a One Day Mortgage™.

This could happen because of an issue with the appraisal or guideline changes made by the lender. Once you’ve chosen your mortgage option, you can see if you’re approved for it. From there, we’ll give you a Prequalified Approval Letter that you can use to shop for homes. For an even stronger approval, you can contact a Home Loan Expert to get a Verified Approval. Apply online for expert recommendations with real interest rates and payments.

Restrictive Covenants: How They Affect Your Property

There are reasons both home buyers and sellers may need to get to closing fast. Getting preapproved means you’re getting the bulk of the mortgage process done upfront. That way, once you’ve had an offer accepted, you can just focus on getting ready for your move. Preapprovals make the house hunting process easier for you and your real estate agent.

Second Home Mortgage Requirements and Rates for 2024 - The Mortgage Reports

Second Home Mortgage Requirements and Rates for 2024.

Posted: Mon, 01 Jan 2024 08:00:00 GMT [source]

Ultimately, final loan approval opens the door to your new home, making understanding these differences essential in your journey to how to get a loan for a house. Remember, exploring loan options with multiple lenders can help you find the best terms suited to your situation. Each of these steps plays a vital role in preparing you for a successful mortgage application.

It's important to note that a pre-approval letter is not a guarantee of a mortgage loan. It provides an initial assessment based on the information provided, but the final approval will depend on additional factors, including a satisfactory appraisal of the property you wish to purchase. It's advisable to maintain open communication with your lender throughout the process and provide any requested updates or additional documentation as needed. "Get pre-approved early. Doing so gives you time to collect the documents you need and especially correct any errors on your credit report," recommends William Seeber from Chicago Financial Services. Start by obtaining a copy of your credit report from one or more of the major credit bureaus (Equifax, Experian, and TransUnion). If your score is lower than desired or you notice any issues on your report, take steps to improve your credit score score before applying for pre-approval.

So that encompasses monthly mortgage payments (principal and interest), property taxes, and homeowners’ insurance, plus any mortgage insurance or homeowners’ association dues. A history of timely payments indicates responsible financial behavior. Conversely, late payments or defaults can negatively impact a lender’s assessment of your reliability. A consistent record of timely payments can positively influence your credit score and your standing with potential lenders, improving your likelihood of loan approval. It involves a more comprehensive review of your finances, including credit checks and verification of your income and debts.

You'll apply for preapproval when you're shopping for homes; you'll apply for approval once you've had an offer accepted on a home. The more verification the lender does for a preapproval, the more likely you are to ultimately receive full approval for a loan in the amount you were originally preapproved for. Your down payment is the amount of cash you pay upfront toward the purchase of a home. Down payments vary in size and are typically expressed as a percentage of the purchase price. A favorable DTI ratio signals to lenders that you’re not overextended with debt and can comfortably manage new mortgage obligations, thus boosting your prospects of getting approved for a home loan.

No comments:

Post a Comment